The PZU strategy was diversified in a manner allowing for both generating stable and predictable cash flows (property and life insurance) and obtaining exceptional profits from complementary operations (asset management and health care).

Investment activity, including in the banking sector, is also a part of the strategy of determining the scale of PZU Group. In the long-term, this approach should allow the shareholders to obtain the expected rate of return from the PZU shares, while maintaing at the same time a moderate level of risk.

Non-life insurance

The aim of the strategy of PZU Group is to strengthen its leadership position on the non-life insurance market in Poland, as well as the improvement of profitability (combined ratio) in this segment.

Retail client

Almost 16 million clients in Poland have put their trust in PZU Group, which is why the retail client segment is an extremely important area for the Group from the point of view of maintaining high level of customer satisfaction, especially by means of appropriate and dynamic adaptation of services and products to rapidly changing needs.

Profitability of non-life insurances (COR)

")

The aim of PZU is to maintain its leading position in the market by improving price and profitability management by channels and strategies of two brands in Poland (PZU and LINK4)

The aim of PZU is to maintain its leading position in the market by improving price and profitability management by channels and strategies of two brands in Poland (PZU and LINK4). The Management Board of PZU intends to implement these goals by means of, for example:

- permanent restoration of profitability of motor insurance and an increase of the activity on the market of profitable non-motor insurance by means of better recognition of the needs of the client and a flexible price policy;

- focusing on maintaining the scale and the growth in internal sales channels (exclusive agents, branches) and improving profitability of external channels by means of better adoption of costs of service to the potential of the distributor and management of profitability in the channels;

- use of the cross-selling potential of PZU Group by means of comprehensive management of PZU Group’s offer (non-life insurance, life insurance, investments, health, and pension) – development of CRM tools supporting all retail sales channels, including direct ones;

- implementation of product innovations on the basis of new technological developments.

Alternative channels for reaching new clients

In order to reach the biggest possible number of retail clients, PZU Group makes use of its two brands – PZU and LINK4 – which have different positions and offers. The complementary offer of LINK4 supports the position of PZU Group in the multiagency channel and on comparison websites. The strategy in this area provides for a systematic exchange of market and organization know-how, including the creation of a joint competence center focusing on price management and an internal innovation center, where LINK4 will function as a low-cost environment for testing new solutions in PZU Group.

In order to reach the biggest possible number of retail clients, PZU Group makes use of its two brands – PZU and LINK4 – which have different positions and offers. The complementary offer of LINK4 supports the position of PZU Group in the multiagency channel and on comparison websites. The strategy in this area provides for a systematic exchange of market and organization know-how, including the creation of a joint competence center focusing on price management and an internal innovation center, where LINK4 will function as a low-cost environment for testing new solutions in PZU Group.

Corporate client

The strategy provides for a dynamic growth of PZU Group in individual business lines within the corporate client segment and Mid-Corpo segment (medium-sized corporations operating on the Polish market). PZU Group will be a business partner with strong expertise that provides its clients not only with insurance products, but also advice, at every stage of risk management process.

It is planned to increase the scale of cooperation with hospitals, local authorities and state-owned companies through development of Towarzystwa Ubezpieczeń Wzajemnych Polskiego Zakładu Ubezpieczeń Wzajemnych (TUW PZUW).

Improvement of PZU Group’s position in the corporate client segment (non-life insurance) will be carried out by means of:

- implementation of system solutions which enable optimal management of the portfolio of corporate clients, including profitability management in the segment and dynamic development of sales of non-motor products;

- dynamic business growth in the Mid-Corpo segment, both in motor insurance and in non-motor insurance (medium- sized corporations operating in the Polish market);

- development of cooperation with hospitals, local authorities and state-owned companies by means of creation of a dedicated insurance coverage offer (almost PLN 500 million in premiums of TUW PZUW in 2020);

- implementation of advanced risk management consulting services (PZU Lab).

Life insurance

As far as the group and individually continued insurance segment is concerned, the aim is to maintain the volume of clients and its high profitability at the level of, at least, 20%, despite strong competition pressure. This objective will be implemented by, among other things:

- active management of profitability within the portfolio of clients;

- development of the offer in terms of products, processes and distribution, with particular emphasis on the SME segment (Small and Medium Enterprises);

- development of service processes applying new technologies and gradual introduction of self-service to group and individually continued insurance;

- increase of the effectiveness of cross/up selling in the scope of property and life insurance;

- development of sales of individual protection life insurance.

Operating margin in group and individual continued insurance

Investments

Asset management for clients

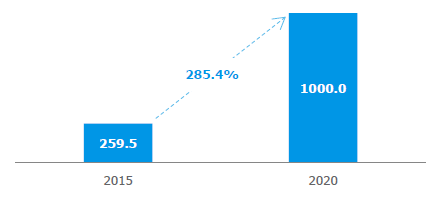

PZU Group’s asset management operations are carried out under the PZU Inwestycje (PZU Investment) brand. PZU wants to become the leader in asset management in Central and Eastern Europe. By 2020, PZU Inwestycje will manage assets worth nearly PLN 100 billion, with the assets of external clients reaching the value of at least PLN 50 billion (TFI and OFE). The contribution of the external asset management business to the financial result of PZU Group will also increase to PLN 200 million. These objectives will be achieved thanks to, among other things:

- new products and widespread availability of the products of PZU Inwestycje in Poland, including through own distribution channels (e.g. Internet);

- providing clients with a possibility of participating in PZU Group’s own investments;

- TFI PZU having a significantly higher share on the Polish market – an increase in the share in the assets of the capital market funds by at least 1 bp each year;

- development by means of sector consolidation in Poland.

A potential purchase of shares in Pioneer Pekao Investment Management SA, Pekao Pioneer PTE S.A. and Dom Inwestycyjny Xelion sp. z o.o. – as one of the consequences of signing the agreement for purchase of Pekao Bank shares – will make it easier to achieve strategic goals of PZU in the scope of asset management. Incorporation of these entities into the structure of PZU Group in 2017 will translate into an increase in assets managed by PZU by about PLN 19 billion.

In the Strategy 2020, PZU Group also sees in the area of asset management a potential to increase savings of Poles. In July 2016, the government announced its Capital Accumulation Programme which is a comprehensive plan to build a voluntary capital savings scheme and long-term investment products in Poland. The program aims to increase the financial safety of Poles, as well as the stability of the public finance system, and to develop local capital market and improve the development potential of the economy. The program includes the creation of universal, voluntary employee and individual capital schemes within the pillar III pension system, public real estate funds, new type of treasury bonds in the form of premium bonds and infrastructure bonds, as well as lowering tax on capital gains from long-term investments (longer than 12 months).

Assets of third party clients under management (PLN bn)

Net result on third party asset management (PLN mln)

In this context, the Capital Accumulation Programme constitutes great potential for implementation of sales of insurance products (the details of this program are to be provided by the end of 2017). If this scenario begins to be implemented, PZU Group will offer its clients attractive and effective investment tools, which will, among other things, make it easier for them to access global markets. PZU Inwestycje is well positioned to become the leader of pension and savings programs.

Investment activity

PZU Group’s strategy in the area of investment also defines the return on the investment of own funds. The achievement of this objective has been quantified as the average annual profitability (by 2020) over the risk-free-rate (RFR) (calculated as the difference between annual, accounting rate of return on deposits invested at the expense and risk of PZU and PZU Życie, that is, among other things, without portfolio of subsidiaries and investment products at the client’s risk, and the average annual level of WIBOR6M).

The increase in investment efficiency, implemented with the assumed level of risk appetite, will be achieved, among others, through:

- greater diversification of the asset portfolio (market, credit, sectoral, geographical and currency diversification);

- optimization of asset classification;

- increasing the efficiency of investment processes determining the medium and long-term shape of the investment portfolio;

- opportunistic use of non-banking niche of enterprise financing (e.g. during M&A transactions) in order to improve the return/risk profile,

- implementation of a new front-office system which allows for the automatic support of the full cycle (except accounting) of asset management.

Surplus of profitablility ratio in own portfolio above RFR

The Strategy was created taking into account the following principles:

- securing the payment of insurance liabilities;

- investment prudence (in accordance with the prudent person principle defined in Solvency II Directive),

- long-term diversification of risk in the portfolio;

- reduction of volatility of the investment result and ensuring stability of the dividend policy.

Health

By 2020, PZU Zdrowie will become the leading integrated coordinated health care operator. This means that it will provide clients with a full range of services in the field of health care. The main objectives in this area of strategy are:

- creation of a comprehensive offer of health insurance supplemented with medical subscriptions and services based on a fee-for-service model;

- providing unique and client-friendly service based on a network of medical establishments, divided according to the parameters of quality and cost effectiveness, supplemented by its own network;

- creation of modern tools of cooperation with a network of subcontractors (portal for the health care providers, development of the assistance system, a communication bus with establishments, and on-line calendars);

- creation of a portal for the client offering self-service functions in an external and own network, and, at the next stage, enabling the purchase of medical services in a nationwide network of PZU Zdrowie by all people insured in PZU Group;

- integration of a network of own establishments and strengthening its market position – promotion of PZU Zdrowie brand and maximization of revenues.

The implementation of these assumptions will be carried out on the basis of:

- development of the offer on the basis of key advantages of PZU Group: a database of 16 million clients, a strong sales network and a high level of brand recognition;

- continuation of the implementation of the acquisition plan – purchase of medical establishments with stable profitability and generating synergy effects (assumptions concerning acquisition costs: PLN 330 million by 2020).

The growing scale of business will be reflected in a systematic improvement of profitability of PZU Zdrowie, and the planned increase in the revenues of PZU Zdrowie will allow it to come significantly closer to the leaders of the private health care market in Poland.

PZU Zdrowie’s revenues (PLN million)

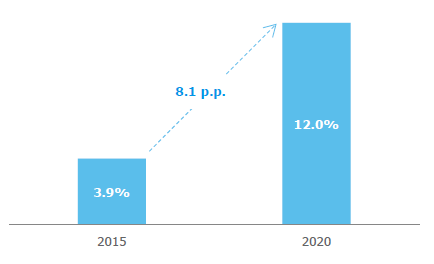

PZU Zdrowie’s EBITDA margin

Banking

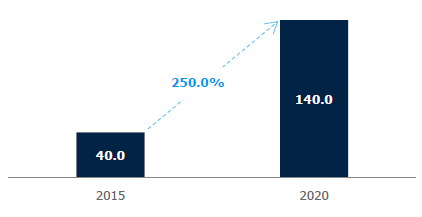

In line with the strategic objectives, by 2020, the contribution of the banking segment to the financial result of PZU Group will increase to PLN 450 million, and bank assets will reach the level of PLN 140 billion. In connection with the announced purchase transactions of a stake in Bank Pekao this measures will be achieved and exceeded already in 2017. PZU Group treats the involvement in the banking sector primarily as a form of investment. The Management Board of PZU is aware of the attractiveness of investment in this sector, in particular in:

- long-term growth prospects (low level of debt in the form of loans, a steady economic growth and stable profitability with moderate risk) and

- low level of consolidation, which provides an opportunity to adopt a strategic market position and build a scale which allows to obtain high rates of return in the long term.

Banking assets (PLN billion)

Net result attributable to the PZU Group in PLN million (banking)

PZU wants to participate in the growth of the Polish banking sector, which is why a project had been developed which included on-going monitoring of possible objectives which could fit within the strategic plans of PZU Group.

Involvement in banks

In accordance with the agreement of 30 May 2015, PZU Group is a shareholder of Alior Bank, with a share of 29.45%. Alior Bank constituted a consolidation platform during the purchase of a part of Bank BPH which included its core operations, without its mortgage loans portfolio and the Investment Trust Company. The agreement for the purchase of shares of Bank BPH was signed on 31 March 2016. PZU supported Alior Bank financially in this transaction as a shareholder. A legal merger of Alior Bank with a separated part of Bank BPH took place on 4 November 2016. Operational merger should be completed in 2017. After the merger, the bank’s assets will amount to approx. PLN 61 billion, which will put Alior Bank on the ninth place in the banking sector. See more

In accordance with the agreement of 30 May 2015, PZU Group is a shareholder of Alior Bank, with a share of 29.45%. Alior Bank constituted a consolidation platform during the purchase of a part of Bank BPH which included its core operations, without its mortgage loans portfolio and the Investment Trust Company. The agreement for the purchase of shares of Bank BPH was signed on 31 March 2016. PZU supported Alior Bank financially in this transaction as a shareholder. A legal merger of Alior Bank with a separated part of Bank BPH took place on 4 November 2016. Operational merger should be completed in 2017. After the merger, the bank’s assets will amount to approx. PLN 61 billion, which will put Alior Bank on the ninth place in the banking sector. See more

In December 2016, PZU announced signing of an agreement with UniCredit concerning a potential purchase of 20% of shares of Bank Pekao (together with the Polish Development Fund (PFR) – 32.8%). Bank Pekao is the second largest bank in Poland in terms of the size of assets. The transaction should be completed in the second quarter of 2017 upon fulfillment of the precedent conditions specified in the sale agreement, which include, in particular, obtaining approvals of antitrust authorities in Poland and Ukraine and approvals or decisions of the Polish Financial Supervision Authority. The aim of PZU is consolidation of Pekao in the financial statements. See more

In December 2016, PZU announced signing of an agreement with UniCredit concerning a potential purchase of 20% of shares of Bank Pekao (together with the Polish Development Fund (PFR) – 32.8%). Bank Pekao is the second largest bank in Poland in terms of the size of assets. The transaction should be completed in the second quarter of 2017 upon fulfillment of the precedent conditions specified in the sale agreement, which include, in particular, obtaining approvals of antitrust authorities in Poland and Ukraine and approvals or decisions of the Polish Financial Supervision Authority. The aim of PZU is consolidation of Pekao in the financial statements. See more

“When the transaction is finalized, PZU will become the largest financial group in Central and Eastern Europe as the leader in insurance, banking and asset management. I am convinced that the existence of such a strong financial institution with the registered office in Warsaw will significantly affect the financial stability and prospects for responsible development of the Polish economy. Thanks to its strength and scale, this institution will have a unique opportunity to create value for our shareholders, clients and employees.” – Michał Krupiński, 8 December 2016

The investment in share package of Bank Pekao constituted for PZU a more effective way of using the surplus capital in comparison with possible return on existing investment activity. The agreed purchase price in the amount of PLN 123 per share was very attractive. The price to book ratio was about 1.3x on the basis of the book value of Bank Pekao (on the date of the planned closing of the transaction). The purchase price was 2.4% lower compared with the price of the sale of 10% stake in Bank Pekao by UniCredit in July 2016 and 3.3% lower than the average price of Pekao shares on the WSE during the last six months (before signing the agreement on 8 December 2016.). It is expected that both ROE and earnings per share (EPS) will increase for PZU Group in 2017- 2018 when the transaction is finalized.

At the same time, with the closing of the transaction concerning the purchase of shares of Bank Pekao, the level of assets from banking activities1, as defined in the 2020 Strategy of PZU Group (PLN 140 billion), will be exceeded, which will result in the revision of the assumptions, in particular in the areas of banking and asset management. Therefore, in 2017, some of the measures of strategy implementation are planned to be updated. See more

Cooperation potential in the banking model

PZU Group is committed to increasing the value of Alior Bank and Bank Pekao. Both bankswill remain separate. There are no plans to combine these two entities because they represent two different business models. Alior Bank is a young, rapidly growing bank which is open to innovation and has ambitions to determine the new directions of development of the Polish banking sector. In contrast, Bank Pekao is the second largest bank in Poland with a long history and a strong capital position, achieving some of the best results in the sector and offering attractive returns from just dividends alone.

PZU plans to generate additional value from these investments also on the level of cooperation in the field of cross-selling of insurance products through a network of branches/clients of Bank Pekao and Alior Bank and asset management, which will result in the revenue growth for both PZU and the banks. The sale of bank products to PZU clients will likely also result in potential synergies. Thanks to these acquisitions, PZU Group will be able to become the leader of diversified financial services in Poland.

|

|

|

|

| Number of clients (in millions) | ~16 million | ~ 5.4 million | ~ 4.1 million |

| Number of branches | 414 | 928 | 1,772 |

1 After the merger with BPH, Alior Bank’s assets plus assets of Bank Pekao amount to about PLN 238 billion.